Major Currencies vs. US Dollar (% change)

08 Aug 2011 – 16 Aug 2011

Talking Points

- EUR: Renewed Selling Likely as Merkel, Sarkozy Dither on EFSF

- GBP: Bank of England Minutes Confirm Dovish Shift on MPC

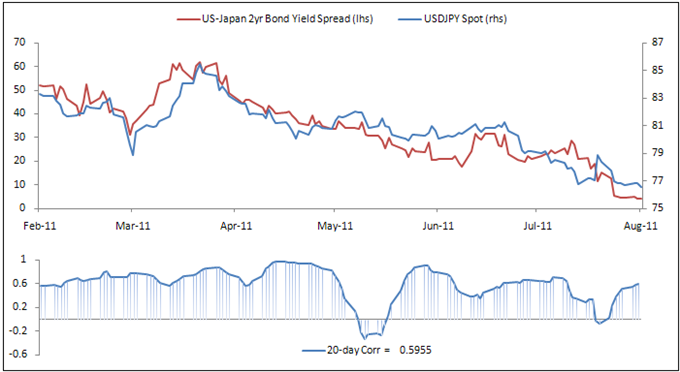

- JPY: Yen Still Caught Between Risk Trends, Intervention Threat

- CAD, AUD, NZD: Stock Markets Continue to Dictate Direction

Currency markets remain firmly anchored to broad-based risk sentiment trends, with most major currencies mirroring investors’ expectations for the evolution of the global economic recovery as reflected in benchmark stock indexes. The Yen is an exception, but here too risk appetite is the key consideration, although its impact is transmitted through a link to Treasury bond yields rather than a direct correlation with share prices (i.e. risk aversion boosts the Yen as capital flows out of equities and into government debt, pushing yields lower and vice versa).

Sizing up the landscape, the recovery in confidence that began at the start of the week appears to be fizzling out as one-off event risks including the Merkel/Sarkozy summit and Switzerland’s rumored announcement of a EURCHF peg pass with little fanfare, leaving little in their wake except the now familiar reality of slowing global growth. New evidence has continued to emerge after the US Empire manufacturing gauge and German GDP figures disappointed while the hawks at the Bank of England abandoned their positions amid increasingly dour conditions. Much was made of a better-than-expected Japanese GDP report, but the nominally smaller drop in output than predicted by economists but the outcome still amounted to the second consecutive print in negative territory, confirming a technical recession the world’s third-largest economy.

Looking ahead, the spotlight falls on the Philadelphia Fed Business Confidence gauge, with expectations calling for another drop in August after a shallow bounce in the previous month. US Consumer Price Index figures will also enter the picture, with headline inflation expected to drop for the first time in seven months. With that in mind, some moderation here was to be expected as oil prices pulled back along with the diminishing outlook for global demand at large. As such the Core CPI figure excluding volatile items (such as energy prices) ought to prove more interesting. This metric is forecast to rise to the highest since November 2009, reinforcing the status quo in the outlook for Federal Reserve monetary policy and keeping a lid on QE3 hopes.

On balance, this opens the door for renewed risk aversion, clearing the way for losses in stocks-correlated currencies against the safe-haven US Dollar. In fact, the greenback ought to begin benefitting disproportionately from safety-bound flows as the only currency not facing the threat of official intervention, as is the case with the Japanese Yen and the Swiss Franc. With that said, speculative short positioning in S&P 500 index futures – a proxy for risk appetite at large – hit the highest level in five months last week, so a deeper upward correction in risky assets is not out of the question in the near term until sellers return in force.

EUR/USD

Key Upcoming Events

| DAY | GMT | EVENT | EXP | PREV | IMPACT |

| 19 AUG | 6:00 | German Producer Prices (MoM) (JUL) | 0.1% | 0.1% | Medium |

| 19 AUG | 6:00 | German Producer Prices (YoY) (JUL) | 5.3% | 5.6% | Medium |

GBP/USD

Key Upcoming Events

| DAY | GMT | EVENT | EXP | PREV | IMPACT |

| 18 AUG | 8:30 | Retail Sales ex Auto Fuel (YoY) (JUL) | 0.1% | 0.2% | Medium |

| 18 AUG | 8:30 | Retail Sales ex Auto Fuel (MoM) (JUL) | 0.4% | 0.8% | Medium |

USD/JPY

Key Upcoming Events

| DAY | GMT | EVENT | EXP | PREV | IMPACT |

| None |

USD/CAD

Key Upcoming Events

| DAY | GMT | EVENT | EXP | PREV | IMPACT |

| 19 AUG | 11:00 | Consumer Price Index (YoY) (JUL) | 2.8% | 3.1% | High |

| 19 AUG | 11:00 | Consumer Price Index (MoM) (JUL) | 0.2% | -0.7% | Medium |

AUD/USD

Key Upcoming Events

| DAY | GMT | EXP | PREV | IMPACT | |

| None |

NZD/USD

Updates on major currency pairs can be learned here.The biggest advantage with forex trading is that here there is no restriction on number of currency pairs in which trading can be done.Financial advisory services like forex trading tips can be referred to earn profitable returns here.

ReplyDelete